》View SMM Metal Quotes, Data, and Market Analysis

》Subscribe to View Historical Price Trends of SMM Metal Spot

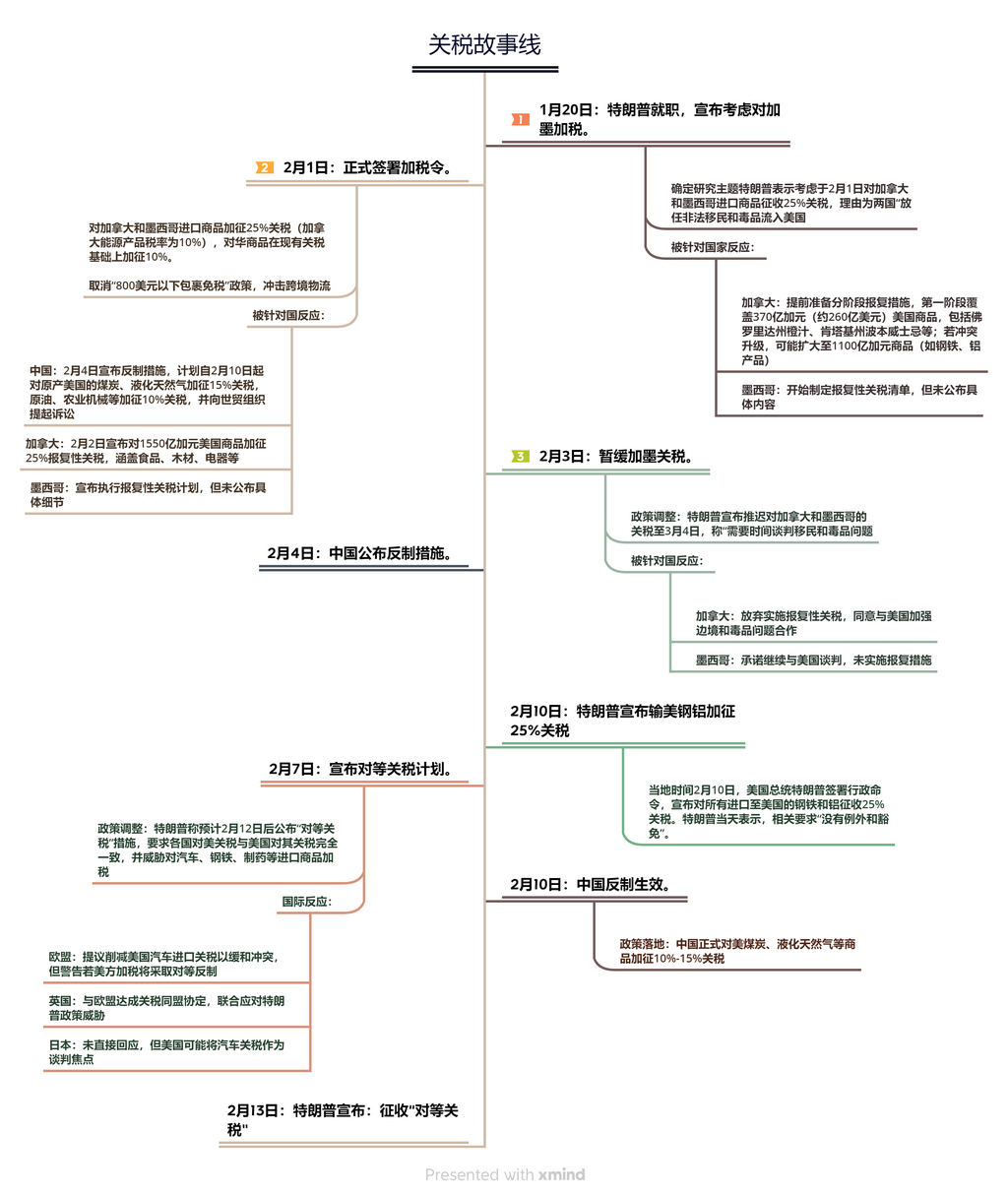

In 2025, Trump proposed multiple tariff hike policies before and after his inauguration, with Canada, Mexico, and China being the primary targets. As early as November 15, 2024, the Ministry of Finance and the State Taxation Administration issued the "Announcement on Adjusting Export Tax Rebate Policies" (2024 No. 15), which canceled export tax rebates for 34 copper semis tariff codes starting December 1, 2024. In February 2025, China officially announced countermeasures.

SMMcompiled based on public information

However, Trump's tariff policies have been inconsistent, making actual implementation unclear, and the US Fed also expressed being "troubled." In September 2024, the US Fed officially entered a new round of interest rate cuts, with consecutive inflation cooling performances boosting its confidence in rate cuts. However, entering 2025, as Trump repeatedly called for "tariff hikes," this topic became a challenge for the US Fed's rate-cutting path in 2025.

Data Source: SMM

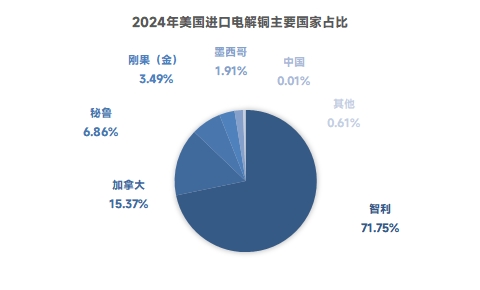

SMMcompiled data on the main countries exporting copper cathode to the US in 2024, revealing that the total share of imports from Canada, Mexico, and China was less than 20%. Subsequently, the US may increase copper cathode imports from Africa, primarily from the DRC and Zambia. If the US officially implements tariff policies related to imported copper, it is expected to boost domestic consumption and African copper cathode import volumes.

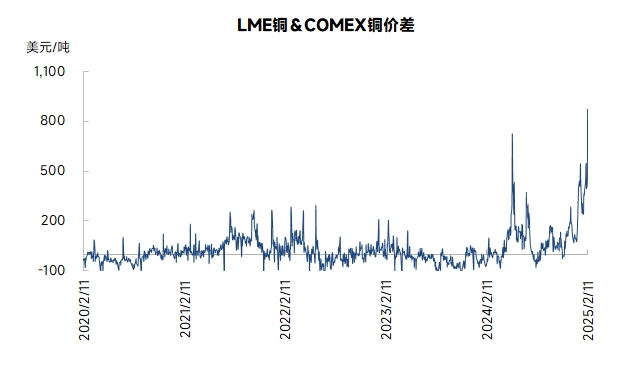

Observing copper price trends, copper prices generally maintained an inverse relationship with the US dollar but showed a stronger positive correlation with gold. COMEX gold repeatedly hit record highs, and COMEX copper prices surged multiple times against the backdrop of rising COMEX copper inventories, showing a significant price spread with LME and SHFE.

Data Source: SMM

Since May 2024, when COMEX copper prices hit a record high due to a short squeeze caused by low inventories, global trade flows have led to a continuous increase in COMEX inventories.

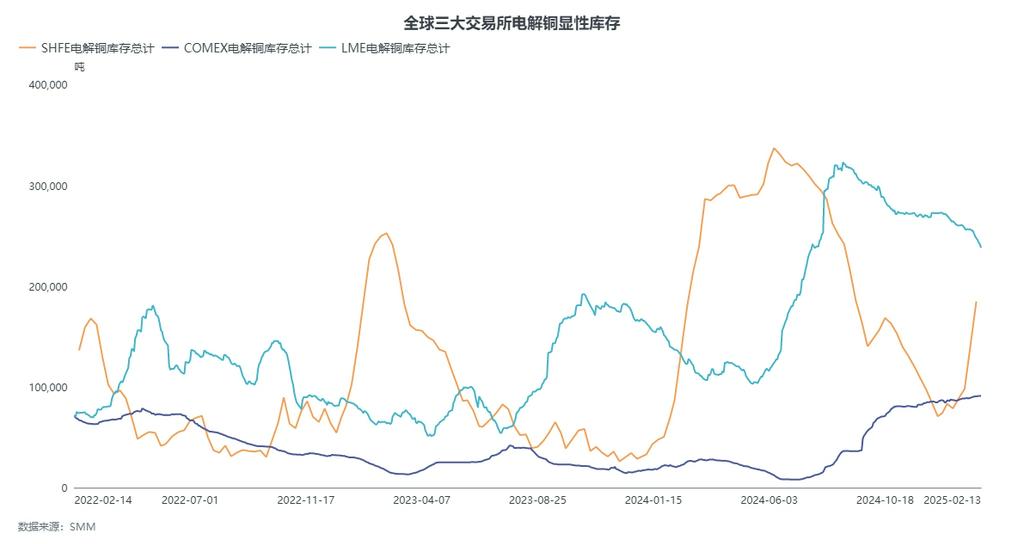

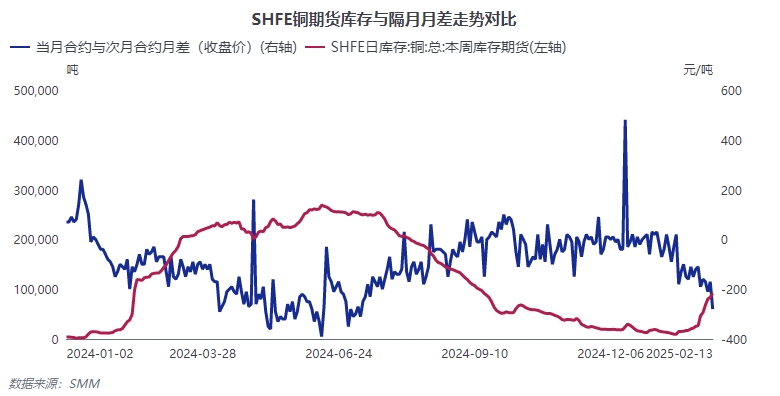

The US Fed's rate cuts, influenced by tariffs, may lead to high inflation. The US dollar has recently faced significant selling pressure due to international market sentiment, while gold and copper have seen rapid price increases. LME followed COMEX's upward trend, while SHFE copper, affected by significant inventory buildup after the Chinese New Year, lagged behind overseas copper price increases. Domestic export opportunities gradually opened, and copper inventories in China's bonded zones increased. However, high copper prices suppressed demand, and SHFE near-month contracts exhibited a significant contango structure, leading to a continuous increase in visible domestic inventories and a notable rise in futures warehouse warrant volumes.

Recently, copper prices surged, while downstream consumption remained weak. Near-month contracts still offer opportunities for reverse arbitrage. For SHFE copper 2502 and 2503 contracts, as the SHFE copper 2502 contract approaches delivery, only short-term or intraday reverse arbitrage opportunities exist. For SHFE copper 2503 and SHFE copper 2504, 2505, 2506 contracts, as well as SHFE copper 2504 and SHFE copper 2505, 2506 contracts, phase-based reverse arbitrage operations remain suitable under the current copper price surge.

Long-term copper prices face risks of jumping initially and then pulling back. Against the backdrop of Trump's potential tariff policies causing the US Fed to hesitate on rate cuts, the Fed's room for further rate cuts is limited. Although the US dollar may pull back in the short term, caution is needed for potential phase-based surges.

During copper price corrections, attention should be paid to supply-demand imbalances in the fundamentals.

Ore Supply: The spot market for copper concentrates continues to collapse, with copper concentrate TC/RC terms further deteriorating. On February 14, the SMM Imported Copper Concentrate Index (weekly) was reported at -$8.67/mt, hitting a new low. The ore supply deficit in 2025 is expected to widen beyond previous forecasts, providing bottom support and phase-based upward momentum for copper prices.

Secondary Raw Materials: The domestic "reverse invoicing" policy continues to impact the pricing model for secondary copper rod procurement to varying degrees. Regarding overseas imports of secondary copper raw materials, the impact of US-China tariffs has prevented import traders from resuming local procurement in the US. Additionally, most US secondary copper raw materials are priced based on COMEX, and the surge in COMEX copper prices has also suppressed the willingness to purchase US secondary copper raw materials. In Europe, local restrictions on renewable resource exports have impacted procurement volumes and costs to varying degrees.

Copper Cathode: From March-June, smelters are expected to undergo seasonal maintenance, leading to tight domestic supply. With recent export opportunities likely to open, smelters may seize the chance to lock in exports. It is reported that major exporters plan to resume export activities in 2025, reducing domestic supply. On the demand side, if copper prices experience phase-based corrections, consumption is expected to improve during the traditional peak season. Copper cathode is entering a destocking phase, supporting changes in futures structures.

Data Source: SMM

Overall, long-term arbitrage operations may lead to phase-based copper price pullbacks. When supply-demand imbalances in fundamentals become prominent, reverse arbitrage profits from earlier stages may transition to positive arbitrage.

》View SMM Metal Industry Chain Database